RRSP vs. TFSA: The Happy Medium Guide (2026 Edition)

The “Too Long; Didn’t Read” Summary:

- Employer Match? Always prioritize the RRSP to get that “free money.”

- Income under $50k? Start with the TFSA. It’s more flexible.

- Have Kids? The RRSP can actually increase your monthly CCB payments (The “Double Refund”).

- The Goal: There is no “bad” way to save. Starting anywhere is better than staying stuck in “analysis paralysis.”

The “happy medium” on retirement savings is knowing enough to make good financial decisions without spending the time, energy, and anxiety on trying to predict the exact most optimal outcome.

RRSPs (Registered Retirement Savings Plan) and TFSAs (Tax-Free Savings Accounts) are two different “containers” for your investments. They both protect your growth from taxes, but they work on a different timeline.

What’s the Same?

- The Tax Shield: Whatever your money earns inside these accounts (interest, dividends, capital gains) is not taxed while it stays in the container.

- The Contribution Room: They both have strict limits on how much you can put in each year.

What’s Different?

- RRSP (Tax-Deferred): You get a tax break now, but you pay taxes when you take the money out in retirement. While you can withdraw anytime, the government treats that money as income today, meaning they’ll take a significant cut for taxes immediately (with a few exceptions like the Home Buyers’ Plan).

- TFSA (Tax-Free): You put in “after-tax” money (no refund now), but you never pay a cent of tax when you take it out. You can withdraw at any time for any reason.

The “Rules of Thumb” for Busy People

If you want a simple direction without worrying about mathematically optimized scenarios, follow these basics:

- The Free Money Rule: If your employer offers a match (e.g., they contribute 3% if you do), max that out first.That is a guaranteed 100% return on your money.

- The $50,000 Rule: If you make under $50,000, the TFSA is usually your best friend. The tax break from an RRSP isn’t as impactful at lower income levels.

- The Refund Rule: If you use an RRSP, invest the tax refund. The “win” of an RRSP only works if you reinvest that extra cash for your future self.

- The Timeline Rule: Retirement savings need to be invested (think ETFs), not just sitting in a savings account. Money in a savings account will not grow enough to beat out inflation. On the flip side, if you need the money in less than 5 years, keep it out of the stock market. Use a GIC or High Interest Savings Account instead.

The Scenarios: What $1,000 Looks Like in 30 Years

To see the real-world impact, let’s look at three common scenarios. We’re assuming a 7% annual return over 30 years and withdrawing the money at the same tax bracket it was earned in.

| Annual Income | Savings Goal | Account Choice | Value in 30 Years | Final Cash (After Tax) |

| $36,608 (Min Wage) | $1,000 | TFSA | $7,600 | $7,600 |

| RRSP (+ $200 refund) | $9,000 | $7,200 | ||

| $60,000 (Median) | $5,000 | TFSA | $38,060 | $38,060 |

| RRSP (+ $1,500 refund) | $49,500 | $34,650 | ||

| $120,000 (High) | $10,000 | TFSA | $76,123 | $76,123 |

| RRSP (+ $4,300 refund) | $109,000 | $76,300 |

Note: The higher your income today, the more the RRSP refund helps bridge the gap, making it the stronger choice for high earners.

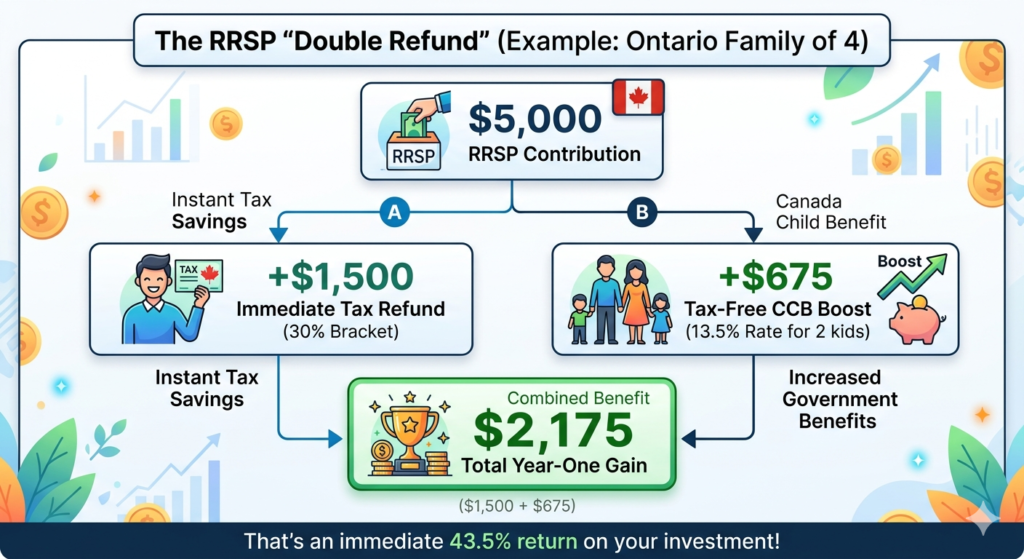

The “Double Refund”: A Secret Weapon for Parents

If you have kids under 18, the RRSP has a secret “lever” that the TFSA simply doesn’t have. It’s all about your Adjusted Family Net Income (AFNI).

Because your Canada Child Benefit (CCB) payments are calculated based on your net income, every dollar you put into an RRSP lowers that number in the eyes of the government. This can trigger a “Double Refund”:

- The Immediate Refund: The standard income tax refund you get after filing your taxes.

- The Monthly Raise: An increase in your tax-free CCB payments starting the following July.

For many Ontario families, this “CCB boost” can add an extra 5% to 20% in value to your RRSP contribution. While a TFSA is great for flexibility, it won’t change your income level, so it won’t help you get more child benefit.

The Bottom Line

The goal isn’t to be a math genius. The goal is to pick a lane and start driving. If you aren’t sure, start with the TFSA—it’s the most flexible ‘Happy Medium’ for most of us. For my guide on setting up a self-directed TFSA through Questrade click here.

Knowing Your Limits: How Much Can You Save?

Before you move a single dollar, you need to know exactly how much “room” you have. Over-contributing to these accounts can lead to a 1% monthly penalty from the CRA on the excess amount—a quick way to kill your “Happy Medium” gains.

1. The RRSP (The “Deduction” Limit)

- The Rule: You can contribute 18% of your earned income from the previous year, up to a maximum cap.

- The 2026 Cap: $33,810. (If you’re catching up for the 2025 tax year, the cap was $32,490).

- The Carry-Forward: If you didn’t max out your RRSP in previous years, that unused room stays with you forever. It’s common for parents to have $50,000+ in “hidden” room they’ve accumulated over a decade.

2. The TFSA (The “Annual” Limit)

- The Rule: Every Canadian resident aged 18+ gets a flat amount of room added every January 1st, regardless of income.

- The 2026 Limit: $7,000.

- The Cumulative Power: If you’ve been eligible since the TFSA started in 2009 and have never contributed, your total lifetime room in 2026 is $109,000.

- The Withdrawal Hack: If you withdraw $5,000 today, you get that $5,000 of room back—but not until January 1st of next year.

Where to Find Your Personal Numbers

Don’t guess! The CRA tracks these numbers for you. Here are the three easiest ways to find your official contribution room:

- CRA My Account: The gold standard. Log in to the CRA My Account portal to see your RRSP and TFSA room side-by-side. Pro-Tip: TFSA room is usually only updated once a year (by April). If you’ve made contributions this year, track them manually!

- Your Notice of Assessment (NOA): Every year after you file your taxes, the CRA sends you an NOA. Look for the “RRSP Deduction Limit Statement” page—it tells you exactly what you can contribute for the following year.

- The TIPS Phone Line: If you prefer the phone, call the Tax Information Phone Service at 1-800-267-6999. You’ll just need your SIN and your last tax return handy.

Have questions about RRSPs vs TFSAs? Message me on Instagram @HappyMediumMoney!