The “$95 Strategy”: How We Turned Half a Gift Budget into $17,000

In late 2016, my now-husband and I were in that “pre-kid” sweet spot. We were both working full-time and had six nephews and nieces we absolutely adored.

But every Christmas and birthday, we hit a snag. He wanted to be generous, and while I appreciated the sentiment, I couldn’t help but notice that our nieces and nephews didn’t seem to lack anything they wanted or needed and I didn’t want to just be buying clutter.

We still wanted them to feel the love and joy of a gift, so we made a deal. We decided to split our gift budget right down the middle:

- Half went to a physical gift they could open now.

- Half went into an investment account to grow throughout their childhood.

At the time, our oldest nephew was 10.

Nearly a Decade of “The Happy Medium”

Fast forward to today. We now have 11 nieces and nephews! As the family grew, we adjusted our contributions. Our goal has always been about $100/year for each child. We started at $50/month, and that has gradually scaled up to $95/month today. Now that our oldest nephew is 19, we’ve decided it’s the right time to gift the money. Going forward, each kid will receive their gift (adjusted for inflation) when they’re 19. We’ll continue contributing until 2039 when we’ll give out the last gift.

Is the math perfect? Honestly, no. Life isn’t a clean spreadsheet. We added more kids, changed the monthly amounts, and we’re about to start withdrawing while others still have 10+ years of growth left.

But here is the real world result of that consistency:

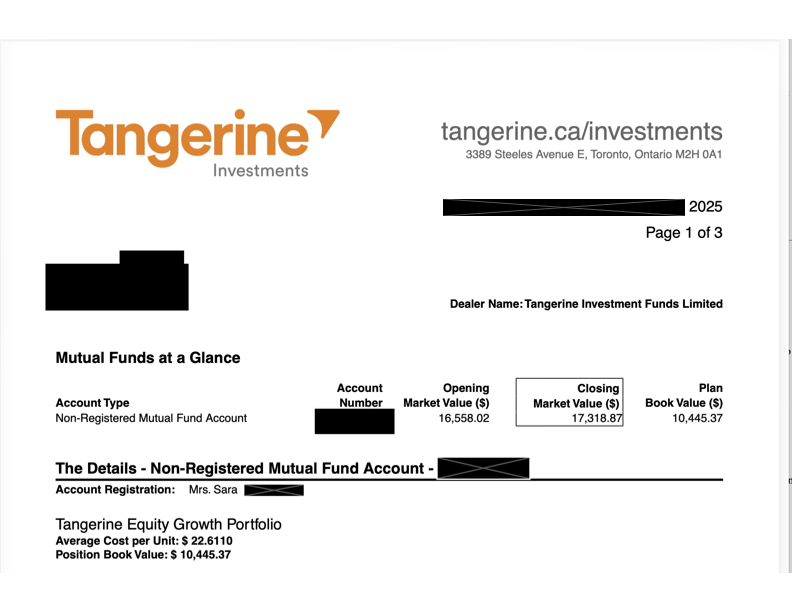

- Total Contributed since 2016: $10,445.37 (including reinvested dividends).

- Current Account Balance: $17,318.87.

By choosing to invest that money instead of just letting it sit in a savings account (or spending it all on toys), we’ve essentially “created” nearly $7,000 of extra gift money out of thin air.

More Than Just a Cheque

What I love most about this is the concrete example it provides to the kids as they enter adulthood. Seeing what their 40-year-old aunt and uncle save for retirement can feel unrelated to their lives. But seeing that carving out just $100 a month could double their money in a decade? That feels reachable. That feels motivating.

To help set them up for success, we’re splitting the gift into a “Financial Sandbox”:

- $1,000 Cash: To do whatever they want with. They’re 19—they deserve some fun!

- $1,000 to Invest: We will help them set up their own account and choose their first investment.

- The $500 Bonus: If they leave that investment untouched for one year, we’ll gift them an extra $500.

It’s a way for them to develop a comfort level with investing that I certainly didn’t have at that age. If they stick with it, they’ll have started a habit that will change their life. If they don’t, it was still a fun windfall!

Why I’m Sharing This

I’m hoping this provides a bit of inspiration. It doesn’t have to be about nieces and nephews.

A decade is a long time, but it’s not forever. $50 a month for 5 to 10 years could make an otherwise “impossible” trip to Europe happen. Maybe you can’t pay for your child’s entire tuition, but saving less, consistently, for a long time will always be a massive help.

Coming up: We’re helping our oldest nephew set up his investment account! I’ll be walking you through the process to show you how you can set up your own TFSA in under 10 minutes to start your own “$95 Strategy.” (And perhaps in another future post I’ll share why the statement pictured above clearly shows my investment was NOT in a TFSA, but I’m fixing that now)

Want to chat about your own strategy? Message me on Instagram @happymediummoney